Sales in the European and German components distribution market are still down on pre-COVID Q1/20 numbers, but as in Q4/2020, order intake went through the roof in Q1/21, according to FBDi.

After a 23% sales boom in the previous quarter, customer bookings went up by 48.8% in Q1/21, signifying a new all-time high of €1.24 billion Euros.

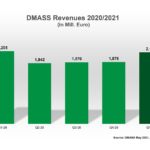

Sales were slightly below expectations at 771 million Euros (-6.1%), held back by the lack of components availability.

At 1.61, Q1 showed the highest book-to-bill rate ever registered at FBDi.

At product level, passive components, which were hit hardest in 2020, increased significantly by 6% to 101 million Euros of sales.

Semiconductors saw a disproportionate decline in some product areas, resulting in a fall of 11% and sales of 501 million Euros.

Revenue with electromechanics were 2.9% higher at 107 million Euros.

Both power supplies sales which were up 8.7% to 32 million Euros and assemblies sales which rose 10.4% to just under 10 million Euros grew comparatively strongly.

Displays and sensors remained in the red, as did semiconductors.

Thus, at least for the first quarter, there was a slight shift in shares. Semiconductors now account for “only” 65% of the cake, passives 13%, electromechanics 14% and power supplies 4%.

Georg Steinberger, FBDi Chairman of the board commented: “Sales development in the semiconductor sector is somewhat disappointing, but in view of a 52% increase in orders to almost 900 million Euros, a rather interesting 2021 is probably ahead, characterised by massive shortages and already foreseeable price increases by the manufacturers. It won’t be much different for the other components.”

FBDi has mixed feelings on the general discussion about Europe’s future role in the high-tech world.

Said Steinberger: “When billions of taxpayers’ money are thrown around for a race to catch up with China, the USA or other countries, one should always ask oneself whether the money is being used correctly. As desirable as a highly subsidised 2-nm semiconductor factory may be for some politicians or large companies, the question arises as how it will benefit the small and medium-sized businesses that shape German and European industry and are defined by lower volume and higher complexity, when it comes to components consumption. From an employment perspective, industrial electronics – encompassing a huge variety of sectors such as automation, medical, energy etc.- are at least as systemically important as the automotive industry. Triple-digit billions must also be amortised, but where are the mass-market applications for this in Europe?”

Comments are closed.