The European semiconductor distribution market has made a sluggish start to 2021, despite a significant increase in bookings since last quarter.

According to DMASS, sales in the European Semiconductor Distribution Market fell by 1.6% to 2.17 Billion Euro. Sequential growth of 15.6% (against Q4/2020) indicates strong turnaround

Georg Steinberger, chairman of DMASS: “While 2020 certainly was influenced by the COVID-19 pandemic and Brexit anxieties, these factors seem to have disappeared completely from the current market development. Now, it is all about components shortage and strategic dependencies on Asian production. Booking levels are crazy and availability has become a revenue-limiting factor for distribution and their customers. The sequential growth indicates the direction the rest of the year might take.”

At a country or region level, the market situation varies significantly and does not show any clear direction.

While Eastern Europe, UK, Italy, Switzerland, Nordic and Benelux showed positive development, Germany, France, Iberia, Israel and Russia declined in the low to high single-digits.

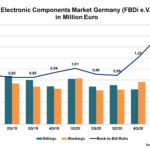

Germany ended with a decrease of 8.7% and 594 Million Euro. France declined by 5.9% to 135 Million Euro, while the UK increased by 8.7% to 143 Million Euro. Italy rose 3% to 212 Million Euro.

Eastern Europe plotted a stable path growing 3.2% to 398 Million Euro and the Nordic region jumped 4.9% to 164 Million Euro.

Adds Steinberger: “Q1 is not really a great trend indicator, considering the major sequential swing and the giant semiconductor shortage, accompanied by significant price increases. As it stands, the current constraints may last well into the later part of 2021, if not beyond.”

Evaluation at a product group level is similarly difficult, and, says DMASS, can be summarised in one word: disparity.

While Discretes, Power and Sensors showed good progress, Opto, Analogue and MOS Micro declined slightly and Programmable Logic, Other Logic and Standard Logic tanked.

Ranked by size, Analogue components declined by -3.8% to 627 Million Euro and MOS Micro nudged down 0.7% to 430 Million Euro.

Power grew by 6.8% to 266 Million Euro, Opto stayed flat with -0.3% to 205 Million Euro and Memories edged ahead 1.2% to 191 Million Euro.

Discretes climbed 14.6% to 130 Million Euro and overtook Programmable Logic, which plummeted 20.5% to 124 Million Euro.

Other Logic fell 13.7% at 105 Million Euro and Sensors advanced 15.7% to 64 Million Euro.

Georg Steinberger surmises: “Funnily enough, some standard products like Discrete and Power did much better in Q1 than Logic in general or Analogue, quite the opposite of last year. However, with a market in turmoil (or boost mode, depending from which perspective you view it) the situation will change during the course of the year. And, as the sequential growth shows, the limiting factor in the coming months may be availability rather than demand.”

“What 2021 will bring is more of what we have seen for a few months, which is over-the- top bookings, price increases, shortage and a reconciliation of procurement strategies to longer-term ordering. The furore with which politics are now trying to tackle the dependency of Europe on Asia when it comes to semiconductor production shows the strategic significance of this technology for many sectors of the European industry. It can be expected that the shift in awareness will not have any short-term impact on supply.”

DMASS claims a coverage of 80 to 85% of European Semiconductor DTAM.

Comments are closed.